Listen to this blog

Revisiting the Mag (Lag?) 7

Summary

In this note we revisit1 concentration in US equity indices. We published our first piece in late February 2024 after AI had captured the attention of the world as an emergent, disruptive technology and propelled US technology shares to new highs. Later in the year, SPX breadth broadened as the odds of a Republican sweep increased with non-technology sectors performing including financials, industrials and small cap stocks expected to benefit from tax cuts and deregulation under a Republican administration.

Below we reexamine: (i) levels of US equity concentration, not much has changed and remains a risk for equities; (ii) the economics and scalability of AI, the technology remains hard to scale and is expensive; (iii) competition in AI and the changing ecosystem; (iv) the potential reframing of US exceptionalism; and (v) spillover risk to indexers, leveraged participants and illiquid assets.

US Equity Concentration

Concentration has risen since we published our first note in February 2024. This includes the rotation underway out of the Magnificent 7 triggered by uncertainty around the Administration’s policies. Macro risks are like a blackhole, for periods of time they exert a smaller force on portfolios but eventually, the force becomes dominant pulling all portfolios into its center. We are in a macro dominant environment. While, ostensibly, the new Administration’s policies are well intentioned, i.e., reshore jobs to America, rebuild American manufacturing, focus on Main Street instead of Wall Street2 , the path to achieve these goals is (very) likely to be long and disruptive. It is also uncertain whether these policies will achieve the desired goals. The result is significant uncertainty for markets and the erosion of animal spirits. We expect this to weigh on equity performance in the coming months. There are equity indices with higher concentration than the US, South Korea with Samsung for example but they cannot match the depth and liquidity of US markets. Global portfolios, particularly indexed portfolios have large exposure to US equities and a widening US equity risk premium will weigh on the performance of these portfolios in the coming months.

Fig 1. Top 7 as % of total Market Capitalization S&P 500. Source: Bloomberg

Economics & Scalability of AI

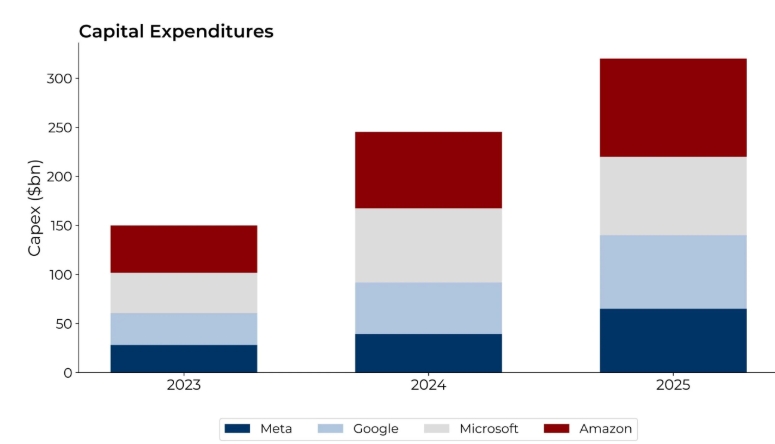

Generative AI is a disruptive technology and will change how we work and innovate. But is it profitable? Generative AI looks nothing like software, a hyper-scaler business model. Software is primarily intellectual property where marginal cost of production approach zero at sufficient scale. At the current technological state, generative AI requires large investments to implement. All the large tech incumbents have dramatically increased capex projections for 2025 in order to invest in the compute required to support training and inference. Collectively, the big four tech incumbents are projected to spend over $315 billion3 on capex in 2025. Unfortunately, for competitive reasons the large technology incumbents are forced to deploy capital and invest in generative AI infrastructure without a clear path to scale and profitability. For example, Sam Altman of OpenAI recently commented how the release of ChatGPT 4.5, which uses chain-of-thought (inference) could not be deployed at scale as a result of compute constraints. OpenAI remains unprofitable as well and is projected to lose roughly $5 billion in 20254.

Fig 2. Capital Expenditure ($ billions). Source: Financial Times

Nvidia is a quasi-monopoly, scales and maintains profit margins over 70%. This cannot last forever and will attract competition. We are already seeing this. Large technology incumbents including Amazon, Meta, Google and Microsoft are designing5 their own GPU chips and contracting with fabs for production. Satya Nadella recently confirmed this in a recent podcast6 explaining how he does not see winner-take-all effects in generative AI. The reason is straightforward, it is risky to have a concentrated dependency on one company, diversifying this risk is prudent and we see competition intensifying both in generative AI models and hardware.

Which brings us to the innovations out of China. The DeepSeek model and paper7 releases triggered a re-pricing of the US AI theme, raising questions about the dominance of US firms in the emergent technology. DeepSeek was started as a research project by a successful China based hedge fund manager, purely out of interest. Working around export controls on the latest chip hardware, DeepSeek researchers were able to find efficiencies both in the training of models and hardware optimization. These efficiencies materially reduce the cost of generating tokens and improve the scalability of the technology. It also undercuts the business models of existing incumbents where part of the perceived moat was ownership and control of prohibitively costly compute infrastructure. DeepSeek chose to open source these innovations and democratize adoption of the technology which further reduces the competitive position of the American firms.

There are historical examples of expensive, disruptive technologies that generated large societal benefits with limited profitability. Examples include canals and railways. Generative AI could be following the same path and market pricing will need to adjust earnings and growth expectations accordingly.

Is US Exceptionalism Over?

America creates many of the world’s best companies, fosters aggressive competition and offers the deepest capital markets in the world. All compelling investment reasons for global savings. The recent deflation of animal spirits and questions around the profitability of generative AI imply a difficult period for US equities. As we mentioned, the Administration’s goals are well intentioned but in order to implement these policies, particularly re-shoring manufacturing to the United States, a cost will be paid in terms of lower asset prices. Tariffs alone inject significant uncertainty into business decisions and are ambiguously negative for risk assets. The cost, both in time and expense of moving production to the United States to satisfy the Administration’s demands creates uncertainty in the planning decisions of many corporations. Although the end result could see a rebuild of the US manufacturing base and strong economic growth, the cost of reaching this goal will be a correction in risk assets. We suspect that US exceptionalism will remain intact but the market adjustment in the coming months will be difficult.

Spillover Risk

If the erosion of animal spirits towards US equities persists, losses and position reduction will continue with many interlinked relationships emerging from the shift in narrative:

1. Potential rebalancing of indexed portfolios away from the United States towards other markets including Europe and China. European and Chinese equity multiples trade at a significant discount to the US. Foreign ownership of US equities currently hovers around 40%8.

2. Rising uncertainty impacts US economic growth prospects. Record tight credit spreads are at risk of significant widening. Rising financing costs will weigh on leveraged corporates. Private credit and equity deals underwritten under optimistic assumptions could face pressure. We will also see a re-marking of private asset valuations if a decline in public equity and corporate bond valuations persists. This could force institutional investors with large private, illiquid asset holdings to sell liquid assets to meet cash flow and liability obligations.

3. De-grossing by leveraged players as losses rise. Losses also dampen risk appetites implying less balance sheet to commit to investment opportunities. We are seeing the early innings of this as crowded themes washout. Position reduction breaks historical correlations, widens various bases and undermines the effectiveness of many hedges, weighing further on losses. We have also seen a rise in the number of firms deploying the pod model, including recent high profile launches. More competition erodes the opportunity set and amplifies de-grossing dynamics. These firms face month-to-month performance pressures, run tight risk constraints and rapidly cut underperforming portfolios.

Takeaways

- US equity concentration remains at record highs. The recent underperformance of the Magnificent 7 has not changed this feature.

- The trajectory of US policy is eroding animal spirits and increasing uncertainty. An unambiguous negative for US equities.

- Generative AI is expensive and has scaling constraints. Large technology incumbents have significantly increased capital expenditure for competitive reasons without a clear path to profitability and scale.

- Markets are re-rating the growth and earnings projections of generative AI lower.

- Competition in generative AI is increasing, both in models and hardware.

- Recent innovations from China have dramatically reduced the cost of tokens undermining the business models of the large American players.

- US players want to diversify their risk to Nvidia and are investing in GPU chip designs to reduce dependencies.

- US exceptionalism is not over, just under pressure. Although the goal of re-shoring manufacturing to the United States is well intentioned, a cost will be paid in terms of lower asset prices.

- Large shifts in perception trigger spillover effects. Candidates include:

- Potential rebalancing of indexed portfolios away from the United States towards other markets including Europe and China.

- Rising uncertainty impacts US economic growth prospects and pressures credit spreads higher. This is negative for leveraged corporates and private asset strategies which rely on leverage. Lower public market valuations lead to a re-pricing of private assets which could pressure asset holders with large illiquid portfolios to sell liquid assets to satisfy liabilities.

- De-grossing at leveraged players. Position reduction breaks historical correlations, widens various bases and undermines the effectiveness of many hedges, weighing further on losses.

1 www.cfm.com/7-reflections-on-the-magnificent-7

2 See Treasury Secretary Bessent

3 www.ft.com/content/634b7ec5-10c3-44d3-ae49-2a5b9ad566fa

4 www.cnbc.com/2024/09/27/openai-sees-5-billion-loss-this-year-on-3point7-billion-in-revenue.html

6 www.youtube.com/watch?v=4GLSzuYXh6w

7 https://arxiv.org/abs/2501.12948

8 See Grok3 estimates

DISCLAIMER

Any statements regarding market events, future events or other similar statements constitute only subjective views, are based upon expectations or beliefs, involve inherent risks and uncertainties and should therefore not be relied on. Future evidence and actual results could differ materially from those set forth, contemplated by or underlying these statements. In light of these risks and uncertainties, there can be no assurance that these statements are or will prove to be accurate or complete in any way. All opinions and estimates included in this document constitute judgments of CFM as at the date of this document and are subject to change without notice. CFM accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. CFM does not give any representation or warranty as to the reliability or accuracy of the information contained in this document. The information provided in this document is general information only and does not constitute investment or other advice. The content of this document does not constitute an offer or solicitation to subscribe for any security or interest.