Listen to this blog

Restoring the American Dream

Restoring the American Dream1

Summary

In this note we examine the large imbalances that have grown between the United States and China since its entry into the WTO, proposed remedies to reduce these balances and how efforts to balance trade will impact financial markets and the real economy. We also discuss China’s deepening capabilities in manufacturing, strong network effects and clustering of key technologies in the manufacturing chain.

Imbalances

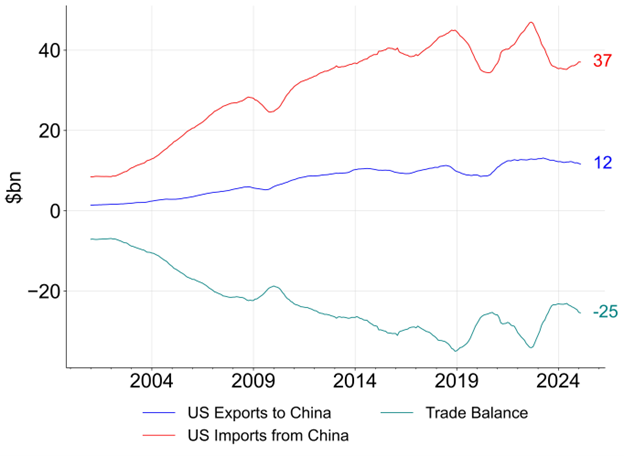

The US runs a goods deficit with China that averages roughly $25 billion a month based on US Census data. China was admitted to the World Trade Organization on December 11th, 2001. Opening China to trade was compelling for several reasons including access to cheap labor to boost the profitability of American corporations and access to the large Chinese domestic market. In 2001, China’s population was approximately 1.27 billion people, the population of the US was roughly 285 million. A closer relationship with China through trading was viewed as a way to strengthen cooperation on strategic and national security issues as well. Finally, it allowed the United States to externalize the cost of pollution, a side effect of a large manufacturing base.

Fig 1. US Goods Imports, Exports and Trade Balance with China in billions of dollars, monthly, non-seasonally adjusted, rolling twelve month average. Source: Bloomberg Finance LP, US Census

Since the early 2000s these imbalances have continued to grow as both the Chinese and US economies have grown richer with nominal GDP rising almost three times in the US and fourteen times in China. China is expected to surpass the US in total output in the near future but on a per capita basis, China has room to catch-up. Currently, GDP per capita is around USD 80k2 in the US versus 13k in China.

Trade imbalances have long been a contentious issue between countries and a politically sensitive topic. The US for example has experimented with high tariffs several times since its founding in 1776. Trade surpluses make countries wealthier. Warren Buffett wrote about this in a 2003 Fortune article3 outlining the problems with America’s trade deficits and proposing a remedy to close them. Using China’s average monthly trade surplus of $25 billion a month, China accumulates $300 billion annually in USD reserves. Brad Setser at the Council of Foreign relations4 puts this number even higher arguing that China has obfuscated its trade statistics5 and financial holdings data6 to report lower numbers. The $300 billion earned by China is reinvested in global financial assets including US equities, Treasuries, and corporate bonds. The United States ‘manufactures’ financial assets to help absorb global savings including wealth created from trade surpluses. As Buffett points out in his article, these are IOUs, claims on the United States where foreigners are lending money to the US to fund its large trade deficits. Running trade deficits allows America to borrow and consume more than it produces. The US has been able to absorb these savings for a long time, benefitting from its status as the world’s reserve currency7, rule-of-law, deep liquid markets and entrepreneurial spirit that has created many of the world’s great companies.

Typically, smaller economies with imbalances are forced to rebalance through market mechanisms that trigger capital flight. Investors sell assets including equities and bonds which pressure the currency lower as capital moves to more attractive opportunities. These adjustments continue until imbalances decline.

In a world where China trades significantly less with the United States, China has less savings to recycle which leads to a decline in demand for US assets. As demand declines, US assets underperform, and investors start to reconsider portfolio allocations and evaluate alternatives.

Foreigners own roughly $19 trillion in US equities, $7 trillion in Treasuries and $5 trillion in US credit. The world is overweight dollar assets with a significant portion unhedged. Historically, the dollar’s role as global reserve currency offered protection to foreign investors as capital moved to safe US assets in periods of stress. Unhedged foreign investors benefitted from this diversification. Estimates8 of European investor dollar hedging demands are $2.5 trillion and $5 trillion for all foreign investors. As hedging increases, the USD will weaken. For example, the 2025 year-to-date performance for an unhedged European investor in the S&P500 is -20%, -10% from the index and -10% from the Euro.

The prevailing policy environment is making it difficult for investors and corporates to plan long term. The short-term equilibrium is to reduce risk or delay investment decisions until investors have more clarity on US policy. Further pressure on the dollar and US assets will continue if large investors including pensions funds and reserve managers decide to rebalance portfolios away from US exposure. On the real economy side, moving production to the United States requires long lead times and low policy volatility in order to make long term investment decisions. If planning is difficult, the immediate response is to wait to make investments in the United States.

Manufacturing

In the early years Chinese manufacturing was low value-add and labor intensive. China invested, learned from competitors, and moved up the value chain, a similar arc to other developing economies. Modern manufacturing in China is competitive, high value-add, achieves significant economies of scale and benefits from technology clusters which reduce transportation costs and drive innovation. For example, China is a leading manufacturer of batteries, electric vehicles, and drones. They are investing in semi-conductor manufacturing, robotics, and AI. If we look at the electric vehicle manufacturer BYD for example, they produce a self-driving EV for less than USD 10k and have reportedly invented a 5-minute charger9 included with more expensive models.

The US has its work cutout to reshore these industries, it will take time and incur significant cost. The Administration’s view that China copied technologies, uses industrial policy and large subsidies to support key sectors and enacts trade barriers to protect domestic markets and industries are valid. This playbook has been used by several developed and developing countries to build competitive industries, China has just executed at much larger scale than anyone in history. China also benefits from an educated workforce including skills in advanced tooling10 and its academic institutions are producing large numbers of STEM graduates. China’s command and control economy also reduces regulatory burdens and allows for rapid building and investment.

The US Administration is moving in this direction and has pledged to reduce red tape, regulatory burdens, permitting and tax burdens to encourage investment and reshore manufacturing. Former President Biden passed the CHIPS and Science Act and the Inflation Reduction Act. Similar to China, both are attempts at industrial policy in the United States. The CHIPS act subsidizes the semi-conductor industry and encourages investment and the IRA targeted investment in green industries including batteries, wind, and electric vehicles. President Trump has criticized both acts and has called for repeals. The President used an executive order to freeze funding to the IRA for example. The Republicans will likely restructure how these subsidies are directed in the coming months.

Remedies

The Administration believes tariffs are a powerful tool to rebalance US trading relationships. Prevailing tariff rates imposed by the Administration are similar to the Smoot-Hawley tariffs that were levied prior to the great depression. The world was significantly less connected in the late 1920s making it difficult to predict how trade linkages will be impacted by current tariffs. For example, roughly 46%11 of US exports rely on imports and if we look at autos, plants operating in the US can import almost half of the components required for production. Effective tariff rates above 20% weigh on trade and in the case of China with rates at 145% trade becomes uneconomic.

The Administration is using these high tariff levels as the anchor point for negotiations and has stated it prefers to get trade deals done with aligned partners first to pressure China to rebalance. In the shorter term it is unambiguously negative for financial markets as tariffs hit spending and earnings, delay investment, increase uncertainty and trigger cascade risks embedded in the complex structure of prevailing trading relationships. The Administration has talked about short term pain for long term gain and appears committed to tariffs to engineer the rebalancing process.

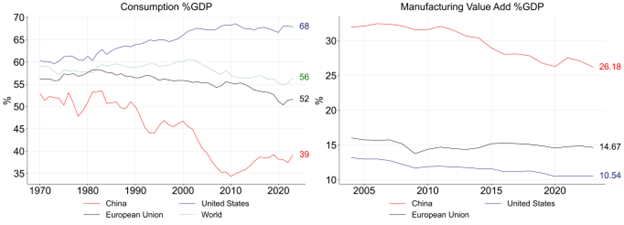

Another solution proposed by Michael Pettis12 is to have China increase consumption. China is the world’s largest manufacturer with roughly 30% of global manufacturing capacity. Instead of exporting its manufacturing surplus to rest-of-world China could stimulate domestic consumption. Currently, consumption in China is around 39% of GDP, well below the US at 70%. Historically, as countries have become richer, they move away from capital intensive manufacturing and shift to a service based economy. By redirecting the manufacturing surplus domestically, China raises less hard currency from its exports and the recycling of savings abroad declines, closing trade imbalances in the process.

Fig 2. Consumption as % GDP (left) & Manufacturing Value Add %GDP (right). Source: Bloomberg Finance LP

Key Takeaways

Restoring the American Dream, as defined by Treasury Secretary Bessent refocuses the United States from financialization, consumption and services to production and the real economy. A new focus on ‘Main Street’ instead of ‘Wall Street.’ The journey to achieve this profound shift is a challenging one but the Administration appears committed to executing its strategy. There are many challenges, the uncertainty and costs of tariffs weigh on planning and investment, building manufacturing capabilities requires long lead times and the skills of the American workforce need to shift to support an American manufacturing renaissance.

- Treasury Secretary Bessent has characterized China as the most imbalanced economy in the history of the world.

- China controls 30% of global manufacturing capacity and is recycling a record amount of hard currency raised from exports into the global financial system creating unprecedented imbalances in savings and trade.

- Running trade deficits allows America to borrow and consume more than it produces. The US has been able to attract global savings for a long time, benefitting from its status as the world’s reserve currency, rule-of-law, deep liquid markets and entrepreneurial spirit that has created many of the world’s great companies.

- In the short term tariffs are unambiguously negative for financial markets. They hit spending and earnings, delay investment, increase uncertainty and trigger cascade risks embedded in the complex structure of prevailing trading relationships.

- The world is overweight US assets, and a significant portion is unhedged. Historically, the dollars’ role as global reserve currency offered protection to foreign investors as capital moved to safe US assets in periods of stress.

- The prevailing policy environment is making it difficult for investors and corporates to plan long term. The short-term solution is to reduce risk or delay investment decisions until investors and corporates have more clarity on US policy.

- Modern manufacturing in China is competitive, high value-add and achieves significant economies of scale.

1 https://home.treasury.gov/news/press-releases/sb0078

2 Bloomberg LP

3 https://fortune.com/2016/04/29/warren-buffett-foreign-trade/

4 https://www.cfr.org/blog/chinas-current-account-surplus-likely-much-bigger-reported

5 China’s National Bureau Statistics has reportedly changed methodologies and data releases.

6 US custodians require ownership disclosure, China has switched custody to other countries (e.g. Luxembourg) which do not require the same reporting requirements.

7 The famous ‘exorbitant privilege’ which allows the US to borrow at lower rates because of large demand for dollars

8 Bank of America

9 https://www.independent.co.uk/tech/byd-battery-charge-tesla-b2731603.html

10 https://www.youtube.com/watch?v=2wacXUrONUY

11Larry Summers interview: https://www.youtube.com/watch?v=b1HGKUPXVh8

DISCLAIMER

Any statements regarding market events, future events or other similar statements constitute only subjective views, are based upon expectations or beliefs, involve inherent risks and uncertainties and should therefore not be relied on. Future evidence and actual results could differ materially from those set forth, contemplated by or underlying these statements. In light of these risks and uncertainties, there can be no assurance that these statements are or will prove to be accurate or complete in any way. All opinions and estimates included in this document constitute judgments of CFM as at the date of this document and are subject to change without notice. CFM accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. CFM does not give any representation or warranty as to the reliability or accuracy of the information contained in this document. The information provided in this document is general information only and does not constitute investment or other advice. The content of this document does not constitute an offer or solicitation to subscribe for any security or interest.